The crypto industry is entering a phase where signing latency has become the binding constraint on participation in on-chain markets. With perpetual DEX volumes surging past $6.5 trillion in 2025 and blockchain finality times collapsing to as low as 100-150ms, the gap between what chains can execute and what custody infrastructure can sign has become a defining bottleneck.

For asset managers running high-frequency strategies across Solana, Hyperliquid, and emerging sub-second chains, every millisecond spent waiting for a key management operation is a millisecond of alpha lost, or worse, a millisecond of unhedged exposure.

This is what we call the latency tax: the invisible cost imposed by legacy MPC protocols and SaaS wallet/custody providers that were designed for a slower on-chain era.

Asset managers can remove the bottleneck while maintaining their standard of security, with self-hosted MPC, such as Sodot. Millisecond-level signing on DKLs23 and FROST is achieved by eliminating the latency heavy network round-trips inherent in SaaS custody models and reducing cryptographic communication rounds to as few as 3, self-hosted MPC collapses the signing bottleneck to near-zero.

The question then is no longer whether asset managers need this speed, but whether they can afford the security compromises that come from pursuing it through shortcuts.

On-Chain Trading Volumes Have Outgrown Legacy Custody Infrastructure

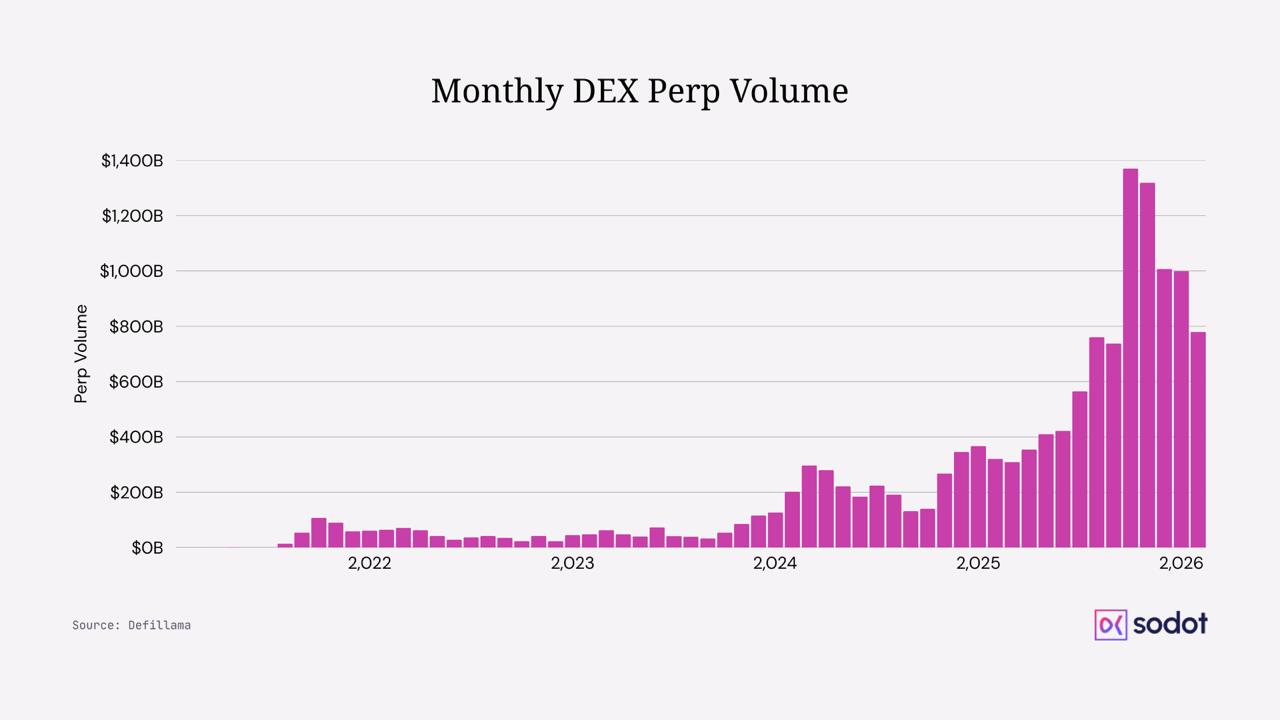

The scale of on-chain trading in 2025 shattered every prior benchmark. Perpetual DEX volumes reached $6.5 trillion for the year, a 2.5x increase from 2024, with monthly volumes first crossing $1 trillion in October 2025. The DEX-to-CEX perpetuals ratio climbed to an all-time high of 11.7% in November 2025.

On the spot side, DEX volumes peaked at $419.76 billion in a single month, and the DEX-to-CEX spot ratio briefly hit 37.4% in June 2025 before settling around 20%.

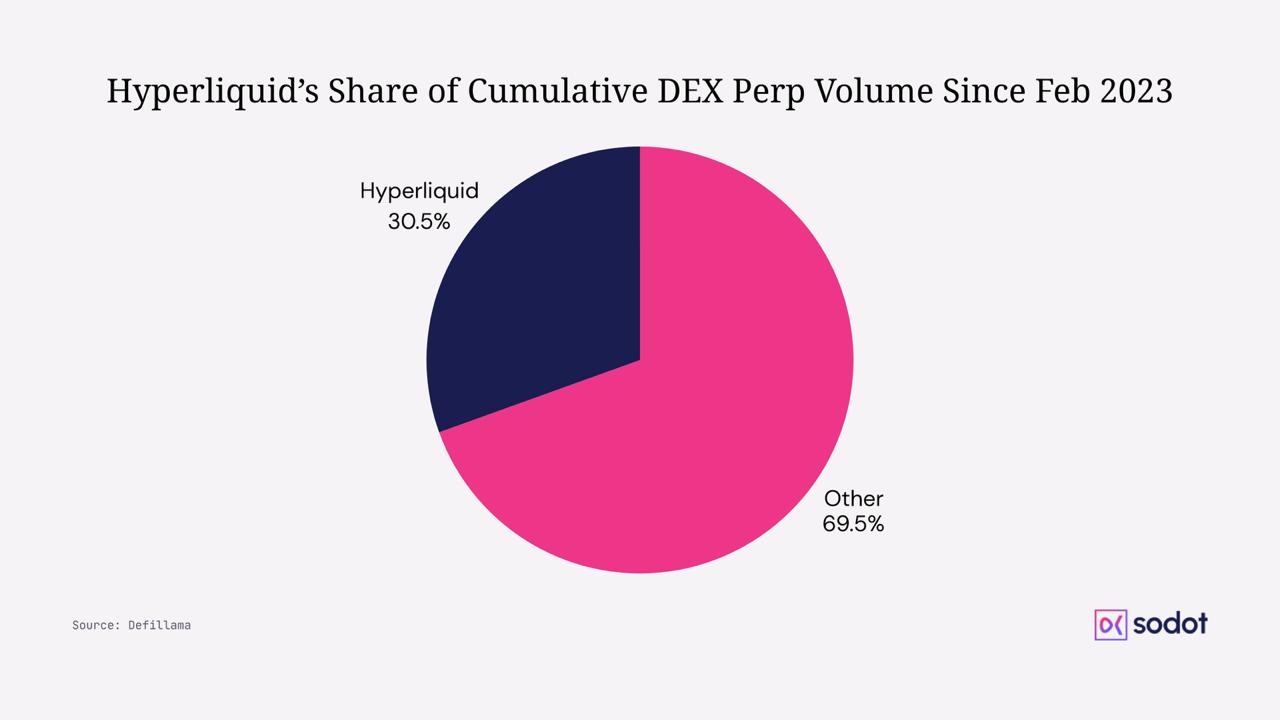

Hyperliquid dominated the perpetual DEX landscape, processing roughly $2.93 trillion in notional volume across 2025, more than double Coinbase's $1.4 trillion over the same period. The platform now handles 200,000 orders per second with a median end-to-end latency of 100ms for co-located clients. Its user base grew from 300,000 to 1.4 million, and open interest peaked at approximately $16 billion.

On Solana, Jupiter captured 93.6% of aggregator-routed DEX volume and processed $264.1 billion in perpetual volume alone.

And these are not retail-driven numbers. The rise of hybrid central limit order book (CLOB) models, which now represent 70% to 92% of total perpetual DEX volume, shows that institutional market makers and quantitative trading firms now operate at scale on-chain.

By the end of 2025, Hyperliquid ranked #7 and Lighter #10 among all global perpetual swap platforms, meaning decentralized venues are no longer a niche alternative to established exchanges, but direct competitors sitting in the same tier.

So, asset managers operating among the world's top 10 perpetual swap platforms face the same execution standards as the most sophisticated players in global derivatives markets, and every operational inefficiency, including custody signing speeds, becomes a measurable drag on performance.

Blockchain Finality Is Collapsing Toward 100ms

The supply side of the latency equation is evolving rapidly, as a new generation of blockchains is explicitly targeting institutional high-frequency trading with finality times that were unimaginable 2 years ago.

The clearest signal of where the industry is heading is Solana's Alpenglow upgrade, approved by 98.27% of validator stake in September 2025. The upgrade replaces Tower BFT with a dual-component architecture:

- Votor, the new consensus layer, introduces BLS-aggregated off-chain voting with a fast path capable of ~100ms finality when 80% or more of the stake participates, with a median across all conditions of ~150ms, and a slow path taking 150–250ms at lower participation.

- Rotor, the new data dissemination protocol, replaces Turbine's multi-layer tree with a single layer of relay nodes that achieves block propagation in as little as 18ms in simulations.

Together, they reduce deterministic finality from 12.8 seconds to roughly 150ms, which is an 85x improvement, while eliminating on-chain vote transactions that currently account for 75% of all Solana activity. Anza confirmed in January 2026 that mainnet deployment is targeting Q3 2026, with Votor deploying first.

Newer chains are pushing even further.

- Fogo, the SVM-based Layer 1 built on Jump Crypto's Firedancer client, launched mainnet on January 15, 2026, with 40ms block times and a curated validator set colocated in high-performance data centers across Tokyo, New York, and London.

- MegaETH, an Ethereum L2 that went live on February 9, 2026, targets 10ms blocks and 100,000+ TPS.

- Monad and Sei both deliver 800ms and 400ms finality, respectively, with parallelized execution pushing throughput into the tens of thousands of transactions per second.

When a chain finalizes in 100ms, a custody system that takes 300ms to produce a signature becomes the bottleneck. At 1,000ms, which is the latency range of legacy GG18/GG20 MPC protocols, the signing infrastructure is an order of magnitude slower than the chain itself. This asymmetry is the latency tax in its purest form.

Quantifying the Latency Tax

This section examines Solana as a case study to quantify the latency tax.

Solana produces one block every 400ms, roughly 2.5 blocks per second. A legacy MPC signing operation takes 1,000ms. In the time it takes to produce a single signature, the chain has already moved on to 2.5 new blocks, each carrying fresh price information that the slow signer never saw. The trader can respond to one out of every 2.5 blocks, while the other 1.5 blocks per second, roughly 3.9 million per month, represent execution windows that simply do not exist for that trader.

So, if the chain produces 216,000 blocks per day (2.5 per second × 86,400 seconds), or approximately 6.48 million per month, a signing system that consumes a full second per operation can participate in at most 40% of them. The remaining 60%, approximately 3.9 million monthly windows, are missed. Each one of those windows carries a price.

Quantifying that price uses the square-root-of-time relationship, where expected price movement scales with √t.

σ per slot = σ annual ÷ √(slots per year)

SOL's annualized realized volatility, calculated from daily closing prices across the full calendar year of 2025, comes in at 86.0%. For 2024, it was 82%, 78.2% for Q4 2025, 75.3% over the trailing 90 days as of early March 2026, and 78.4% over the trailing 365 days.

At 86% annualized volatility and 78.84 million slots per year (one every 400ms, running 24/7/365), the expected price movement per slot is:

0.86 ÷ √78,840,000 = 0.000097 = 0.97 basis points per slot

Every block that a trader's signing infrastructure forces them to skip carries, on average, a 0.97 basis point adverse price shift.The figure is consistent with established academic research. The Loss-Versus-Rebalancing framework developed at Columbia and a16z (Milionis et al., 2022) demonstrates that adverse selection costs in automated market making scale directly with σ² × block interval, meaning shorter block times and higher volatility both amplify the penalty for being slow.

A 2025 follow-up paper proved that Solana's deterministic block schedule actually minimizes aggregate LVR compared to stochastic alternatives, but for individual traders, the per-block cost remains the binding constraint.

The practical cost depends on how many additional blocks a trader misses due to signing latency. A legacy system taking 1,000ms to sign while a high-performance alternative completes in under 100ms creates a differential of roughly 900ms, or 2.25 additional blocks at 400ms per slot.

Not every one of those missed blocks results in adverse selection. Some fraction of the time, the price happens to move favorably or not at all. Under conservative assumptions where approximately 40% of trades encounter adverse price movement from a 1.5-block average delay, the cost per trade works out to:

1.5 missed blocks × 0.97 bps × 40% adverse frequency ≈ 0.58 bps per trade

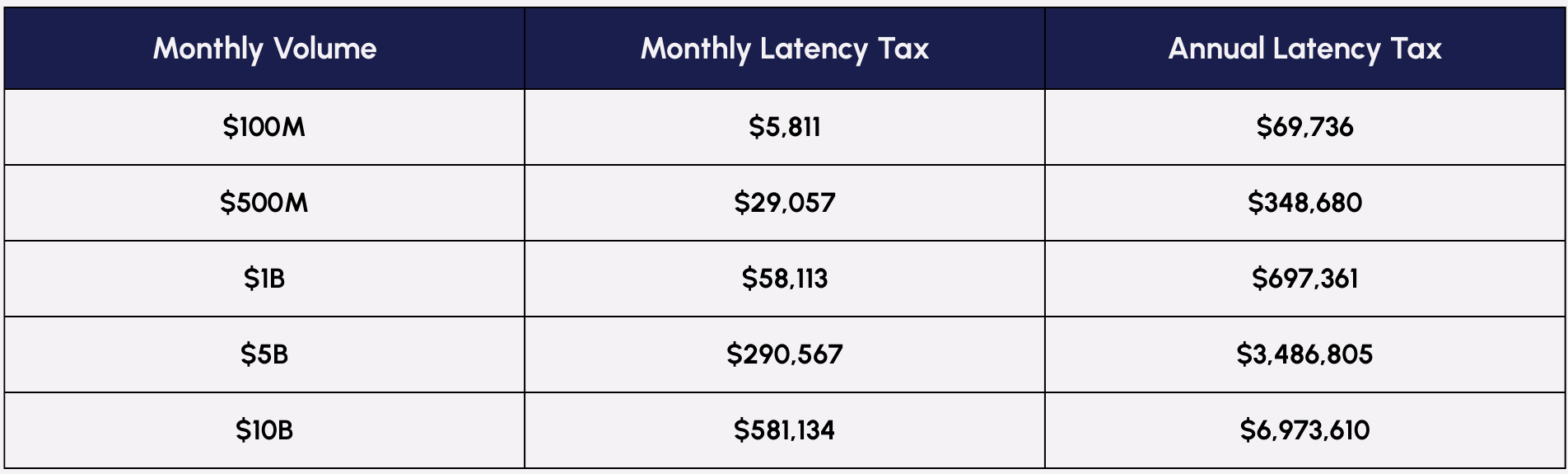

Applied across monthly trading volume, the dollar cost scales linearly:

And the figures are, if anything, conservative. They assume a single-asset volatility regime of 86%.

During concentrated volatility episodes like Q1 2025, when SOL's annualized vol spiked to 111%, the per-slot cost rises to 1.25 bps, pushing the annual tax on $1 billion in monthly volume above $900,000.

The calculation also excludes second-order effects: the MEV exposure from stale orders sitting in mempools (Helius documented $142.8 million in successful arbitrage extractions on Solana in 2024 alone), the compounding cost of missed hedging opportunities across correlated positions, and the opportunity cost of strategies that simply cannot be deployed at all when signing latency exceeds the chain's native cadence.

For example, Jito processed over 3 billion bundles in 2024 with $674 million in tips. A single sandwich bot operator extracted $13.4 million in 30 days with an 88.9% success rate across 1.55 million transactions. Chorus One's research found that Jito's auction window is just 200ms, meaning any participant slower than 200ms is excluded from the most profitable execution opportunities entirely.

The cost compounds further under Alpenglow. Although the upgrade does not change Solana's 400ms block cadence, it collapses deterministic finality from 12.8 seconds to approximately 100-150ms.

Today, a slow signer's stale quotes become exploitable relative to optimistic confirmations that still carry reversion risk. Post-Alpenglow, those same stale quotes will be exploitable relative to the fully finalized state, removing any ambiguity about whether the price move is real. Every participant on the network will know, with cryptographic certainty, that the price has moved, within 150ms of it happening. A signing system that takes 1,000ms to authorize a response will be operating against confirmed reality.

MPC Protocol Evolution Maps Directly to Signing Speed

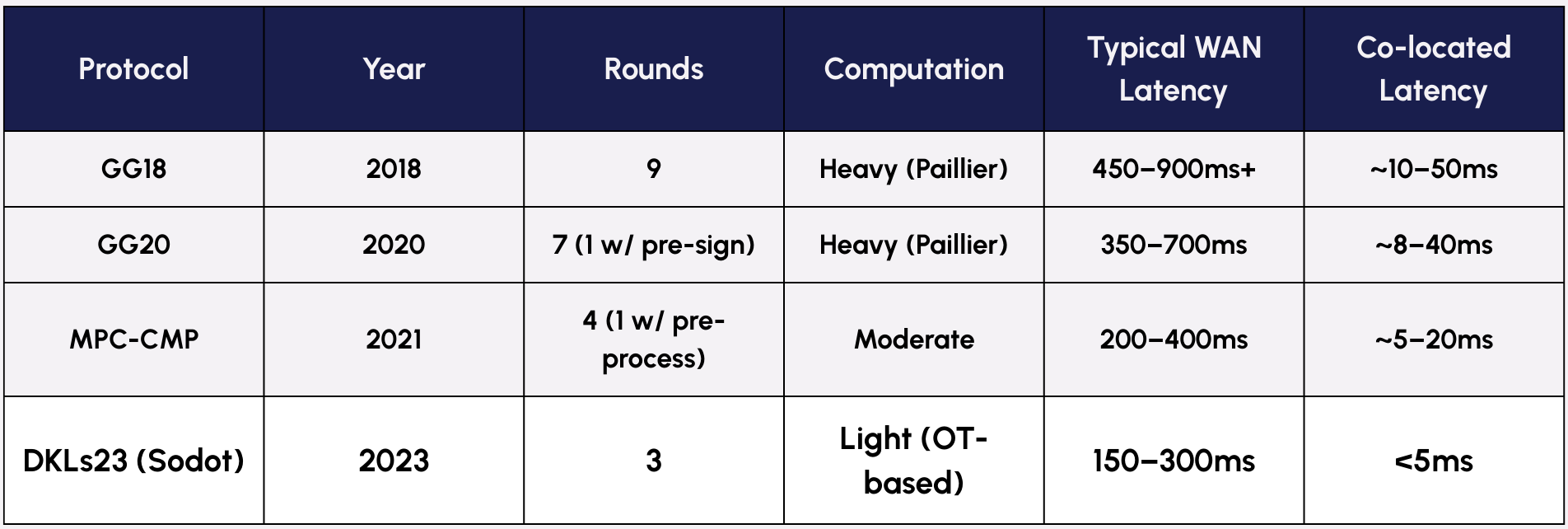

The history of threshold ECDSA protocols is fundamentally a history of reducing communication rounds, because each round of interaction between MPC key shares introduces a full network round-trip of latency. Over wide-area networks, a single round-trip typically costs 50–100ms. Over local-area networks or co-located infrastructure, it can drop below 1 millisecond.

The original GG18 protocol required 9 rounds of communication between signers, translating to 450–900ms of pure network overhead over WAN, plus computational time for Paillier encryption operations.

GG20 reduced this to roughly 7 online rounds (or 1 with pre-signing), but retained the heavy Paillier arithmetic. Fireblocks' MPC-CMP (CGGMP21) was a solid improvement: 4 rounds online, or 1 round with pre-processing, achieving an 8x speedup over GG18 and earning broad institutional adoption. In 2025, Fireblocks released MPC-BAM, a 2-party protocol claiming ~100x improvement over older configurations.

On the other hand, Sodot's core ECDSA protocol, DKLs23, requires only 3 rounds of communication and uses oblivious transfer (OT) rather than Paillier encryption, making it computationally lighter, an advantage that compounds on resource-constrained devices like mobile phones.

For EdDSA (Solana, Aptos, Sui) and Schnorr (Bitcoin Taproot), Sodot implements FROST, which offers similar round efficiency. Over co-located infrastructure, round-trip times drop below one millisecond, which means three-round MPC signing adds roughly 1ms of network overhead on top of sub-millisecond computation. The total signing latency lands in the low single digits, sub-5ms in Sodot's implementation, where server-to-server signing within the same data center leaves the network as a non-factor.

The self-hosted deployment model is what makes this achievable. When MPC key shares reside within a customer's own cloud infrastructure, such as running inside TEE (Trusted Execution Environment) secure enclaves on AWS, Azure, or GCP, the network path between shares is measured in microseconds rather than the tens or hundreds of ms required for round-trips to a SaaS provider's external infrastructure. This is the fundamental latency advantage of self-hosting: it converts WAN-scale round-trips into LAN-scale ones.

$4 Billion in 2025 Losses Prove Security Cannot Be Traded for Speed

The temptation to cut security corners for performance is understandable, but also catastrophically dangerous. Across 2025, the crypto industry lost $4.04 billion to theft and exploits, according to Peckshield. North Korea's Lazarus Group alone accounted for $2.02 billion, achieving this with 74% fewer known attacks than prior years, executing fewer but far more devastating operations.

The Bybit hack of February 21, 2025, the largest cryptocurrency theft in history at $1.4–1.5 billion, is the perfect example. The attack was not a cryptographic failure. Bybit's multi-signature cold wallet operated correctly at the protocol level.

Instead, Lazarus Group compromised a developer at a third-party signing interface, injecting malicious JavaScript that replaced legitimate transaction data with a contract upgrade call while displaying the original transaction to signers. All three required signers approved what they believed was a routine cold-to-warm wallet transfer. The multi-sig did exactly what it was designed to do. It collected the required signatures, but the human-interface layer between the cryptographic ceremony and the signer's understanding was the vulnerability.

Unfortunately, this pattern repeated across the year's other major incidents. Phemex lost $73 million across 16 blockchains simultaneously in January 2025. Nobitex lost $80–90 million in hot wallet compromises. The Coinbase insider breach exposed 69,461 users' data through bribed overseas support contractors, an outsourcing-for-speed decision that created insider threat vectors. Cetus Protocol on Sui lost $223 million to an arithmetic overflow in a faulty overflow check (checked_shlw) in the shared integer-mate math library, which allowed the u256 shift-left operation to silently corrupt liquidity accounting.

And yet, no major MPC wallet provider has suffered a cryptographic breach in production. The failures occur at the interface layer (Bybit), the key storage layer (Phemex hot wallets), and the operational layer (Coinbase insiders).

Properly implemented MPC with distributed key shares across isolated systems, independent transaction verification channels, and self-managed policy enforcement addresses each of these vectors by ensuring that the speed of signing does not come at the cost of verification integrity.

Sodot's Architecture Eliminates the Signing Bottleneck Without Compromising Custody Guarantees

Sodot's infrastructure is built around a specific thesis: that self-hosted MPC can deliver both institutional-grade security and latency characteristics compatible with high-frequency on-chain trading. The company has assembled a client roster that includes eToro, BitGo, Exodus, Flow Traders, Flowdesk, and Bitcoin.com, collectively representing tens of billions in secured assets.

The core product, Sodot MPC Infra, deploys a server-side component called Vertex within secure enclaves, paired with client-side SDKs for Kotlin, Swift, React Native, Unity, and WASM. The self-managed policy engine runs entirely within the customer's infrastructure. Sodot holds no key shares, participates in no signing operations, and has zero visibility into customer data.

Because the signing infrastructure runs on the customer's own servers, Sodot's availability as a vendor has no bearing on customer operations. In a SaaS custody model, the vendor adds latency and introduces a single point of failure. Here, it does not.

The Dynamic MPC feature allows custodians to change the number of shares (n) and signing threshold (t) without changing public keys or blockchain addresses. A treasury team can transition from 2-of-3 to 3-of-4 signing when adding a team member, or rapidly reconfigure after a share loss, without the costly and risky process of migrating assets to new addresses. SOC 2 Type 1 and Type 2 audits from EY, cryptographic code audits from Trail of Bits (September 2024) and NCC Group (September 2025), and TEE-based execution ensure none of that operational flexibility comes at the cost of security.

The Exchange API Vault, launched January 29, 2026, with Flow Traders as one of the first integrators, extends the security model to centralized exchange API keys and custodian API keys. The product provides centralized control over key creation, permissioning, and real-time enforcement with a built-in kill switch, while maintaining the low-latency characteristics that institutional market makers require. API key exploits contributed to multiple 2025 incidents, and the Exchange API Vault closes that vector without introducing the operational friction that typically accompanies tighter key controls.